If the borrower defaults, the lender takes the home. In today's tech-savvy world, many mortgage loan providers and brokers have automated the application process. This can be a big time-saver for hectic households or experts as they stabilize choosing the very best home loan, looking for a home and their everyday lives. Some loan providers even offer apps so you can use, monitor and handle your loan from a mobile device.

At a glance, it can be frustrating. It's constantly great to browse different loan providers' websites to familiarize yourself with their loan products, published rates, terms, and lending process. If you choose to apply online with very little face-to-face or phone interaction, search for online-only lending institutions. If you work with a bank or cooperative credit union, check online to see what items and conditions they provide.

As you search online, you'll undoubtedly encounter providing marketplaces or personal finance sites that recommend particular lending institutions. Bear in mind that these sites usually have a limited network of lenders. Likewise, they generally make cash on referrals to loan providers featured on their website. So don't rest on those suggestions without doing extra shopping by yourself.

Looking into and educating yourself before you start the process will give you more confidence to method lenders and brokers. You may need to go through the pre-approval procedure with a few lenders to compare home mortgage rates, terms, and products - why do holders of mortgages make customers pay tax and insurance. Have your documents organized and be frank about any obstacles you have with credit, income or savings so loan providers and brokers offer you products that are the very best match.

Conforming loans fulfill the fundamental certifications for purchase by Fannie Mae or Freddie Mac. Let's take a closer look at exactly what that means for you as a customer. Your loan provider has two options when you validate a home mortgage loan. Your lending institution can either hang onto your loan and gather payments and interest or it can sell your loan to Fannie or Freddie.

Most lenders offer your loan within a couple of months after near ensure they have a consistent capital to provide more loans with. The Federal Real Estate Finance Firm (FHFA) sets the rules for the loans Fannie and Freddie can purchase. There are a number of fundamental criteria that your loan should meet so it complies with acquire requirements.

Facts About How Do Reverse Mortgages Work When You Die Uncovered

In many parts of the contiguous United States, the maximum loan quantity for an adhering loan is $484,350. In Alaska, Hawaii and specific high-cost counties, the limitation is $726,525. In 2020, the limitation is raising to $510,400 for an adhering loan. In Alaska, Hawaii and specific high-cost counties, the limit is raising to $765,600.

Your loan provider can't sell your loan to Fannie or Freddie and you can't get an adhering home mortgage if your loan is more than the maximum quantity. You'll require to take a jumbo loan to money your home's purchase if it's above these restrictions. Second, the loan can not already have backing from a federal government body.

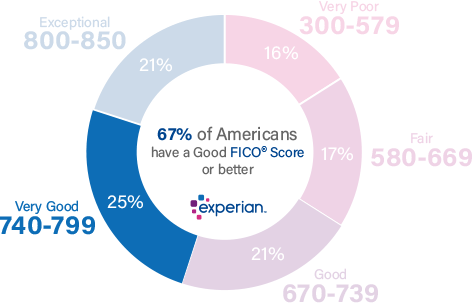

If you have a government-backed loan, Fannie and Freddie may not purchase your home loan. When you hear a lending institution talk about a "adhering loan," they're referring to a conventional home mortgage only. You'll likewise need to satisfy your lending institution's specific criteria to certify for a conforming home loan. For example, you need to have a credit report of a minimum of 620 to get approved for a conforming loan.

A House Loan Professional can assist determine if you certify based on your special financial circumstance. Adhering loans have distinct standards and there's less variation in who gets approved for a loan. Since the loan provider has the option to sell the loan to Fannie or Freddie, adhering loans are likewise less risky than jumbo loans (what are the main types of mortgages).

A conventional loan is a conforming loan moneyed by private financial lending institutions. Traditional mortgages are the most typical type of mortgage. This is since they don't have stringent regulations on income, house type and home place certifications like some other types of loans. That stated, traditional loans do have more stringent guidelines on your credit rating and your debt-to-income (DTI) ratio.

You'll likewise require a minimum credit report of at least 620 to certify for a traditional loan. You can skip buying personal home mortgage insurance coverage (PMI) if you have a deposit of at least 20%. Nevertheless, a deposit of less than 20% implies you'll require to pay for PMI.

10 Easy Facts About How Much Are The Mortgages Of The Sister.wives Described

Conventional loans are an excellent option for a lot of customers who don't receive a government-backed loan or wish to make https://www.businesswire.com/news/home/20190723005692/en/Wesley-Financial-Group-Sees-Increase-Timeshare-Cancellation the most of lower rate of interest with a bigger deposit. If you can't offer a minimum of 3% down and you're qualified, you might consider a USDA loan or a VA loan.

The amount you pay monthly might fluctuate due to changes in local tax and insurance rates, however for one of the most part, fixed-rate mortgages provide you a really predictable month-to-month payment. A fixed-rate home mortgage may be a better option for you if you're currently living in your "permanently home." A set rates of interest provides you a better concept of how much you'll pay every month for your mortgage payment, which can assist you budget plan and prepare for the long term.

When you secure, you're stuck with your rate of interest for the period of your mortgage unless you re-finance. If rates are high and you secure, you might pay too much thousands of dollars in interest. Speak to a regional genuine estate agent or House Loan Expert for more information about how market rates of interest trend in your location.

ARMs are 30-year loans with rates of interest that alter depending upon how market rates move. You initially concur to an initial period of fixed interest when you sign onto an ARM. Your initial period might last between 5 to 10 years. During this introductory period you pay a fixed interest rate that's usually lower than market rates.

Your lender will take a look at a fixed index to figure out how rates are altering. Your rate will https://www.inhersight.com/company/wesley-financial-group-llc go up if the index's market rates go up. If they go down, your rate goes down. ARMs consist of rate caps that dictate just how much your rates of interest can alter in an offered duration and over the life time of your loan.

For instance, interest rates may keep increasing year after year, but when your loan hits its rate cap your rate won't continue to climb. These rate caps also go in the opposite instructions and restrict the amount that your interest rate can decrease as well. ARMs can be a great choice if you prepare to purchase a starter house prior to you move into your permanently home.

What https://bestcompany.com/timeshare-cancellation/company/wesley-financial-group Does How Many Lendors To Seek Mortgages From Do?

You can quickly take advantage and save money if you do not prepare to live in your house throughout the loan's complete term. These can also be specifically advantageous if you plan on paying extra toward your loan early on. ARMs start with lower interest rates compared to fixed-rate loans, which can give you some additional cash to put towards your principal.